11% Yield With Zero STRC Risk. Meet Saturn Protocol.

Saturn Credit. $105M TVL in 6 weeks. Incubated by YZi Labs

11% Yield With Zero STRC Risk. I Had to Check How That’s Possible.

Saturn Credit. $105M TVL in 6 weeks. Incubated by YZi Labs

May 20, 2026

Saturn Credit. $105M TVL in 6 weeks. Incubated by YZi Labs (Binance Labs). Backed by Spartan Group and Susquehanna. Saylor featured the founder at Strategy World Conference -- not a retweet, the actual conference stage. And the weird part -- their stablecoin has zero STRC exposure. The yield comes from STRC dividends, but USDat holders never touch it.

I am pulling it apart. Here’s everything -- how it works, the 5 layers of DeFi strategies built on top, the structured credit mechanics nobody’s explaining, the risks at every layer, and whether the farming math actually worth it

If you’re not a fan of reading, you can watch this video where I also break it down part by part:

Ready? This is a long one. Grab a coffee.

First, You Need to Understand $STRC

You can’t understand Saturn without understanding what it’s built on.

What is Strategy Inc?

Strategy Inc (formerly MicroStrategy) is a Nasdaq-listed company that pivoted from enterprise software to becoming a Bitcoin treasury company. Their playbook: raise money through capital markets, buy Bitcoin, hold it forever.

The problem: how do you keep raising money to buy more Bitcoin without diluting your common shareholders (MSTR holders)?

STRC -- The Money Machine

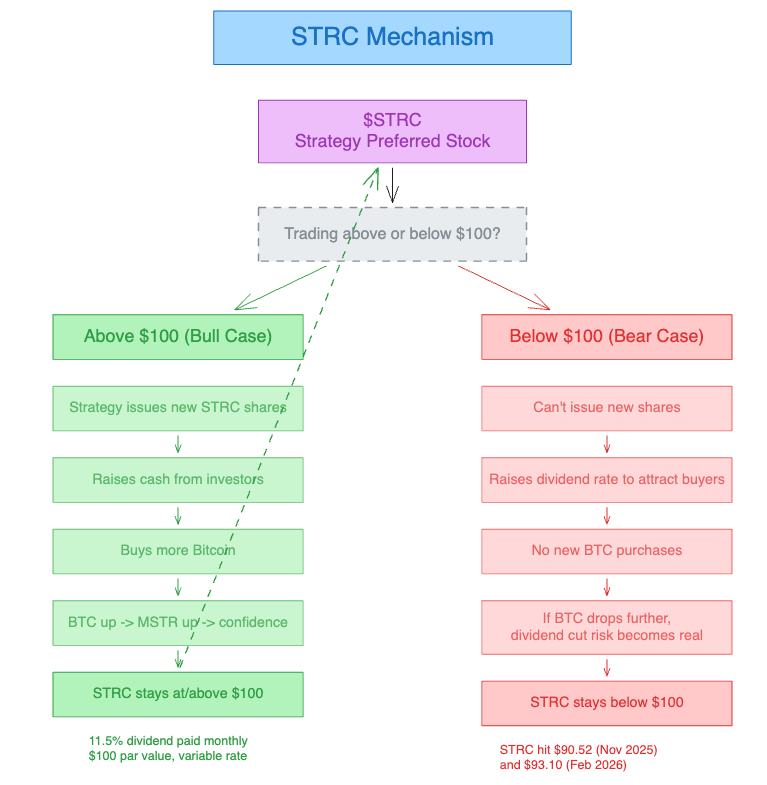

$STRC is Strategy’s Variable Rate Series A Perpetual Preferred Stock. Think of it like a bond that never matures but pays dividends forever.

Par value: $100/share. Strategy wants STRC to trade near $100

Dividend: ~11.5% annually, paid monthly in cash. 100 shares ($10K) = ~$1,150/year, ~$96/month

Variable rate mechanism: Strategy adjusts the dividend rate monthly based on 30-day VWAP and SOFR. Below par = raise rate to attract buyers. Above par = can lower it

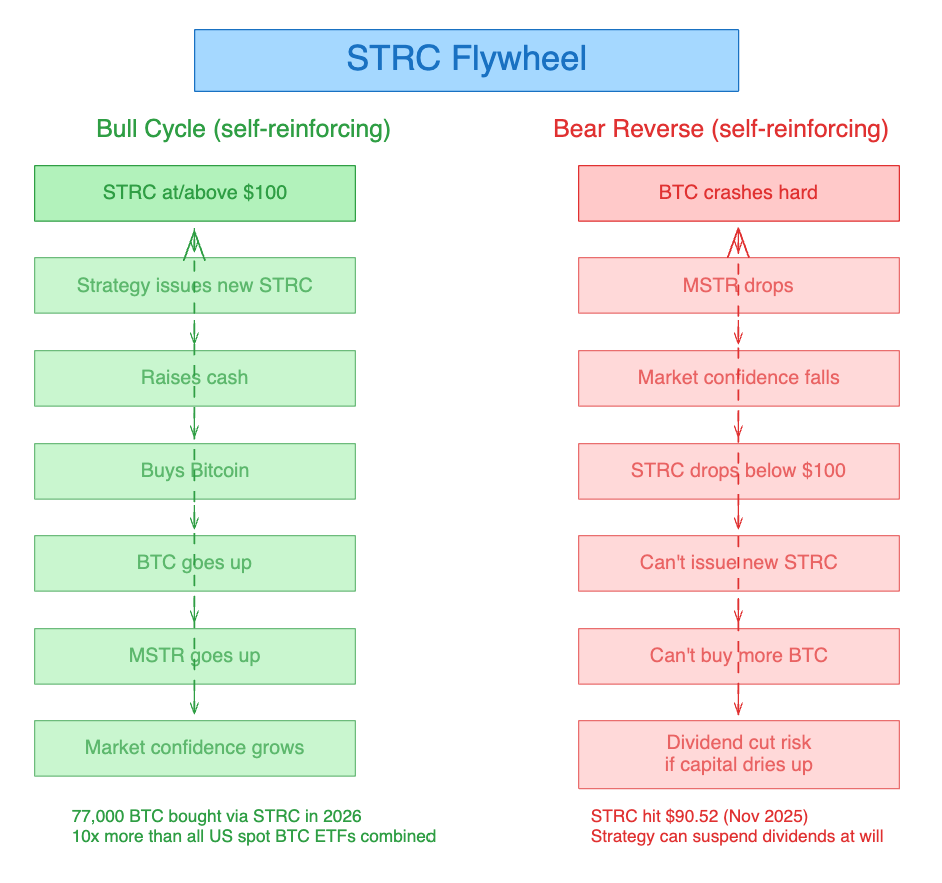

Capital raise mechanic: When STRC trades at/above $100, Strategy issues NEW shares and uses proceeds to buy Bitcoin. No MSTR dilution

The Flywheel in Reverse

BTC crashes hard -> MSTR drops -> Market confidence falls -> STRC drops below $100 -> Can’t issue new STRC (nobody buys below par) -> Can’t buy more BTC -> BTC narrative weakens further -> Possible dividend cut if capital dries up.

STRC has traded as low as $85-$95 during stress periods. The dividend is “an economic tool, not a legal guarantee” -- Strategy can reduce, suspend, or delay it. STRC holders rank junior to all debt.

Bottom line on STRC: High-yield preferred share (~11.5%) from a company that is essentially a leveraged Bitcoin bet. Yield is real and paid monthly, but only flows as long as Strategy’s BTC-fueled capital machine keeps working.

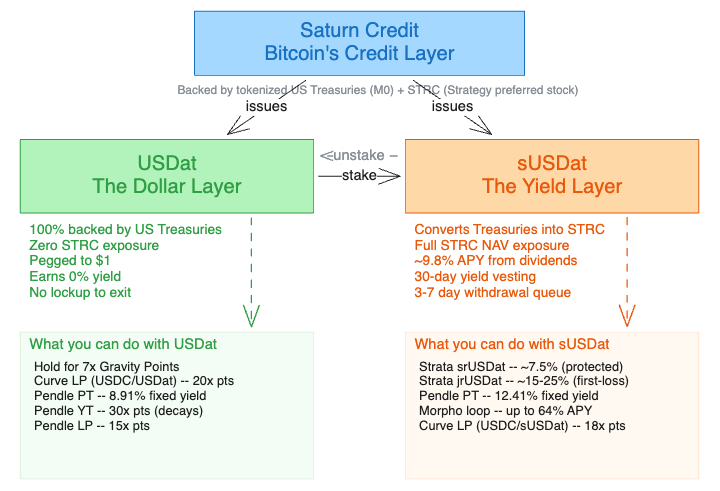

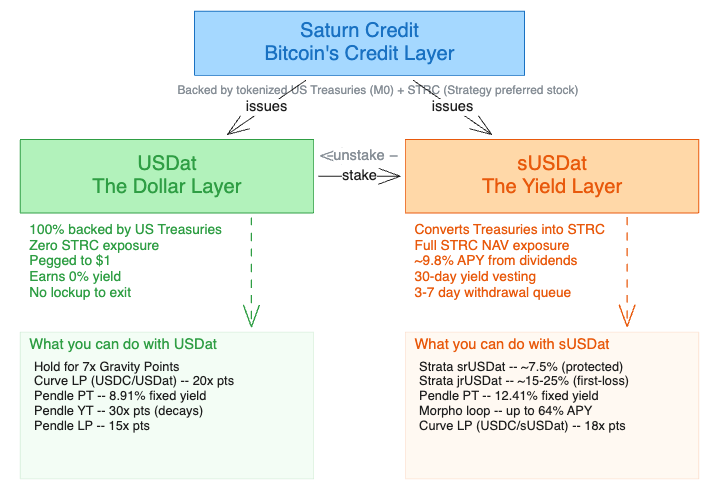

What Saturn Actually Does

Saturn’s design philosophy is clean separation between the stable layer and the yield layer. This is the key architectural difference from other STRC tokenizers.

USDat -- The Dollar Layer

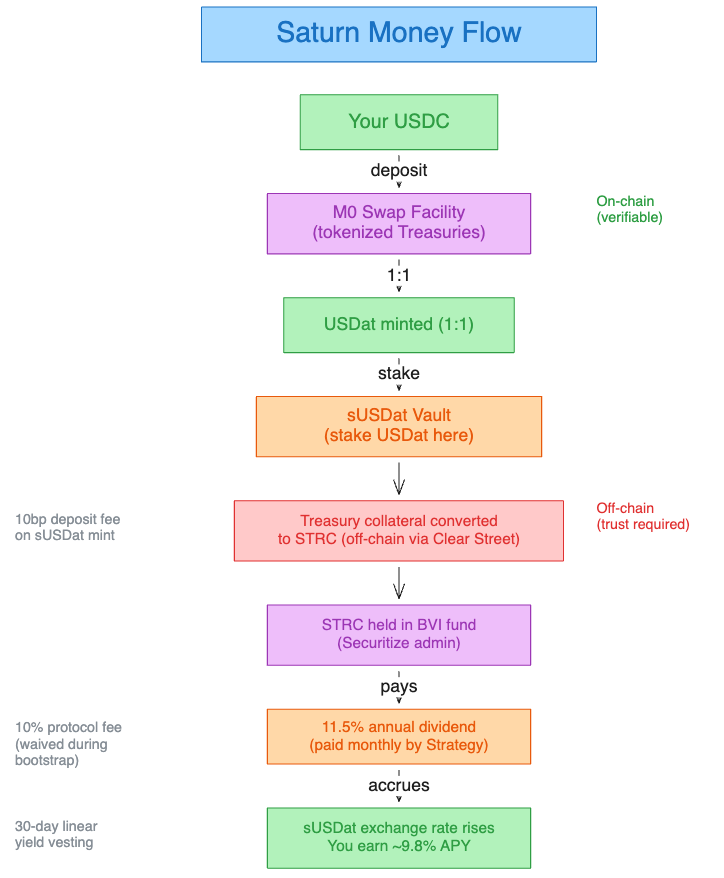

A stablecoin backed 100% by tokenized US Treasuries via M0’s $M product.

Backed by T-bills, not STRC. USDat holders have zero exposure to STRC price risk

Market cap: ~$105.7M

Designed to trade at $1

Minting: deposit USDC or $M through M0 Swap Facility at 1:1. Requires whitelisting

Redemption: USDat -> Wrapped $M (1:1) -> Uniswap V3 swap (1bp fee) -> USDC

Non-onboarded users access USDat through Curve pools

Earns zero yield from STRC. Purely a stable settlement layer

sUSDat -- The Yield Layer

The ERC-4626 vault token where actual yield lives. When you stake USDat into sUSDat, the underlying Treasury collateral is converted into STRC exposure.

Current APY: ~9.8% (May 2026). Target: 11%+

Yield from STRC monthly dividends. sUSDat exchange rate rises as dividends accrue (like wstETH)

30-day linear vesting on rewards to prevent front-running

10bp deposit fee on sUSDat minting

10% protocol fee on yield (currently returned to holders during bootstrap)

3-7 day withdrawal (3-stage process: request -> processor sells STRC -> claim via NFT)

Key risk: if STRC falls in price, sUSDat experiences the same drawdown

Where the Yield Actually Comes From

Let me trace the full chain.

You deposit USDC. Saturn mints USDat through M0 (backed by Treasuries). You stake USDat into sUSDat. Protocol converts Treasury collateral into STRC. STRC pays 11.5% annual dividends monthly. Dividends accrue to sUSDat exchange rate. You earn ~9.8%.

Not emissions. Not funding rates. Corporate dividends from a Nasdaq-listed company.

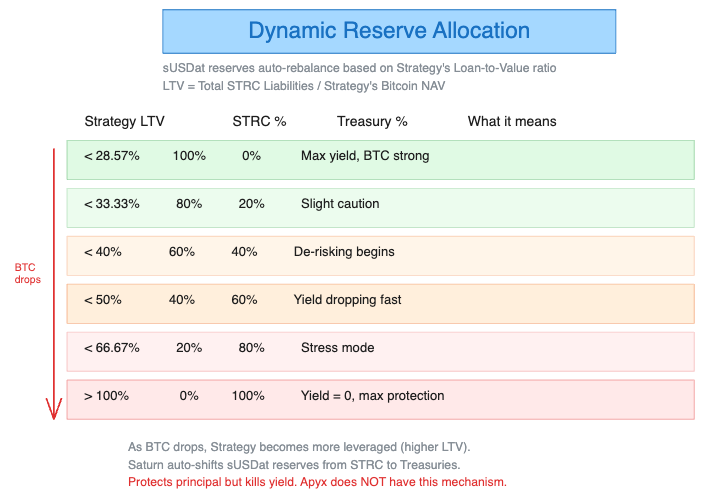

The Auto De-Risking Nobody Talks About

Saturn dynamically rebalances between Treasuries and STRC based on Strategy’s Loan-to-Value ratio. As BTC drops and Strategy becomes more leveraged:

LTV <28.57%: 100% STRC (max yield)

LTV <40%: 60% STRC, 40% Treasuries (de-risking begins)

LTV <66.67%: 20% STRC, 80% Treasuries (stress mode)

LTV >100%: 0% STRC, 100% Treasuries (yield = 0, max protection)

This means as things get ugly, Saturn automatically shifts your reserves to safety. Yield drops to zero but your principal is protected. Other STRC tokenizers don’t have this. In the next stress event, this difference matters.

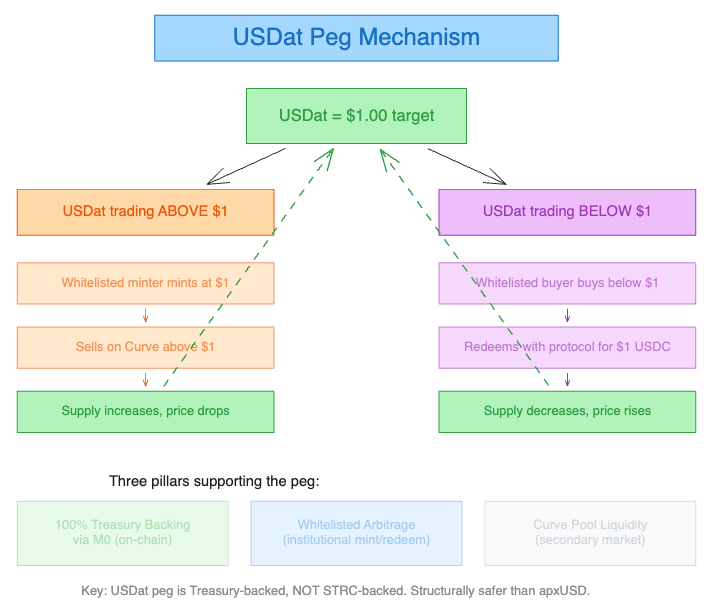

How USDat Keeps Its Peg

Three mechanisms:

1. 100% Treasury backing. USDat is fully backed by tokenized US Treasuries via M0. Not fractional reserve. Every USDat is redeemable 1:1 for USDC.

2. Whitelisted arbitrage. Institutional participants mint at $1 and sell above, or buy below $1 and redeem with protocol for $1.

3. Curve pools. Non-whitelisted users trade USDC/USDat on Curve. Market makers keep the pool balanced.

What breaks the peg:** USDat is Treasury-backed, so peg risk is lower than STRC-backed stablecoins. Main risk is smart contract failure or M0 infrastructure failure, not STRC price movement.

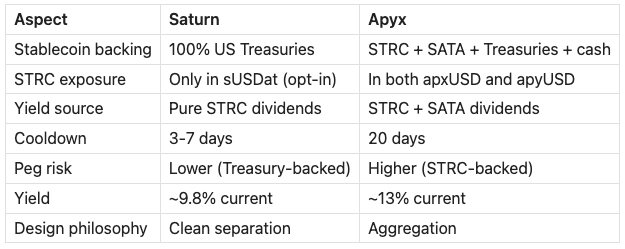

Saturn vs Apyx -- The Design Difference

Saturn’s USDat is a genuinely different product. USDat holders have zero STRC downside. The tradeoff: lower yield, smaller ecosystem.

The Saylor Connection

Saylor featured Saturn’s CEO Kevin Li at Strategy World Conference. Strategy’s official X account published Saturn content. Strategy’s website hosts a video: “New Market Structures Using STRC & Bitcoin-Linked Products: Saturn.”

This is deeper than retweets. Saylor RT’d Apyx 4x -- that’s notable. Saturn got the conference stage and the official channel. Whether that translates to anything contractual is unknown, but the optics signal strategic alignment.

Saturn is building a DeFi demand layer for STRC. Strategy benefits because every dollar flowing into Saturn is ultimately buying STRC on the open market, supporting the par value, and enabling more Bitcoin purchases. The incentives are aligned.

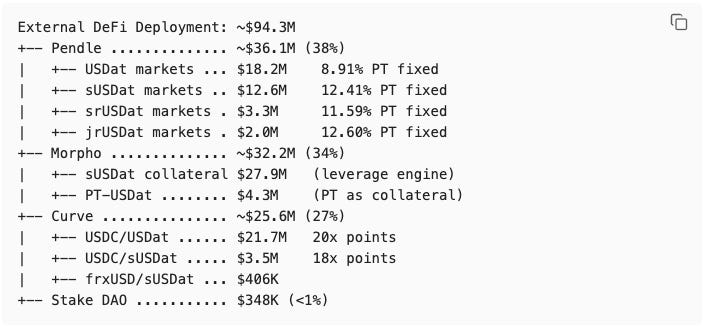

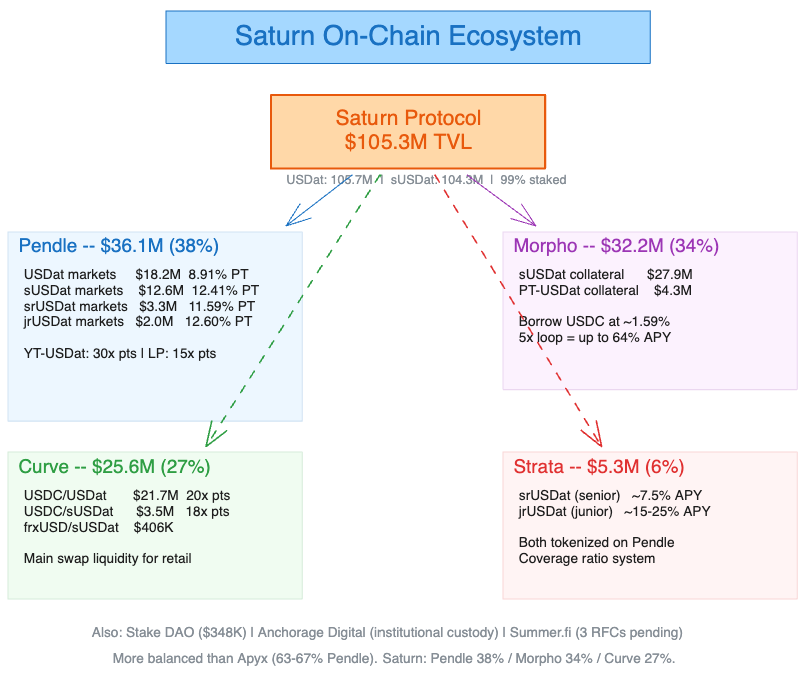

Where USDat and sUSDat Live On-Chain

$105.3M TVL. The breakdown matters more than the headline.

105.7M USDat minted, backed by $105.3M in M tokens (tokenized Treasuries). 104.3M sUSDat total supply -- meaning 99% of all USDat has been staked into the yield layer. Almost everyone opted into STRC risk.

More balanced than Apyx (which has 63-67% on Pendle). Saturn: Pendle 38% / Morpho 34% / Curve 27%. Healthier distribution -- less dependent on a single venue.

The 5 Layers of Saturn DeFi Strategies

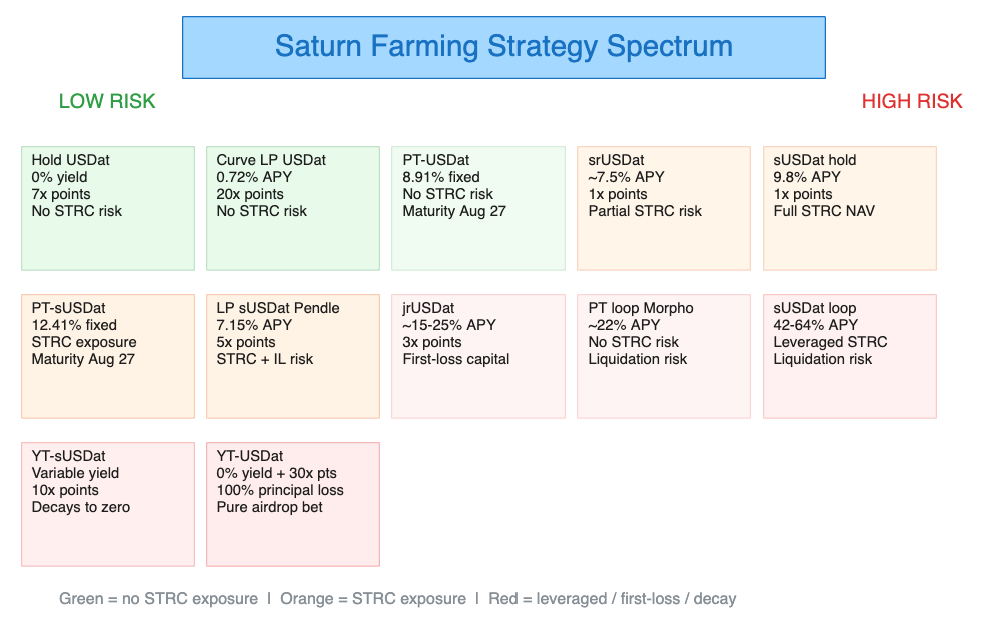

This is where it gets interesting. Saturn’s ecosystem has 5 layers, each building on the one below. From simple to complex, from safe to degen.

Layer 0: Saturn Protocol (Base Layer)

Action Yield Risk Points Mint USDat 0% Near zero (Treasury risk only) 7x Stake USDat -> sUSDat ~9.8% STRC NAV exposure 1x

USDat is safe but earns nothing. sUSDat earns ~9.8% but you take STRC price risk. Almost everyone (99%) has chosen sUSDat.

Layer 1: Curve (Swap Liquidity + LP)

Pool TVL APY Points USDC/USDat $21.7M 0.72% 20x USDC/sUSDat $3.5M 49.9% 18x

Curve USDC/USDat at 20x is the highest non-YT points multiplier. Since both tokens peg to $1, IL is minimal. You’re farming points on a stablecoin pair. Lowest complexity way to farm hard.

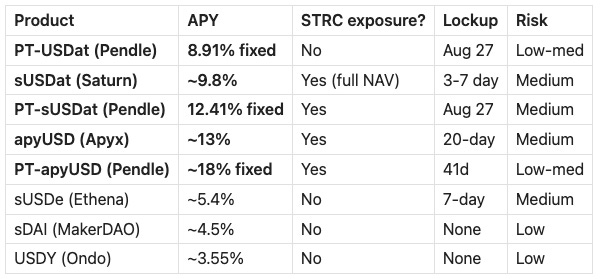

Layer 2: Pendle (Fixed Yield + Yield Speculation)

Pendle splits any yield-bearing token into two pieces. PT (Principal Token) = buy at discount, redeem at full value at maturity. Your “fixed rate” play. YT (Yield Token) = captures all variable yield until maturity, then expires at zero. Your “leveraged yield bet.”

Market PT fixed APY YT Points LP Points Maturity USDat 8.91% 30x 15x Aug 27 sUSDat 12.41% 10x 5x Aug 27 srUSDat 11.59% 15x 7.5x Aug 27 jrUSDat 12.60% 10x 5x Aug 27

PT-USDat at 8.91% is the standout. Discounted USDat that redeems 1:1 at maturity. Underlying is T-bills, not STRC. Zero STRC NAV risk. 8.91% fixed for ~3 months. That’s 2x what any T-bill fund pays.

YT-USDat at 30x is the degenerate play. You buy the yield stream of USDat (which is 0% base yield -- purely farming points). Your entire principal decays to zero at maturity. Need the airdrop value to exceed what you paid.

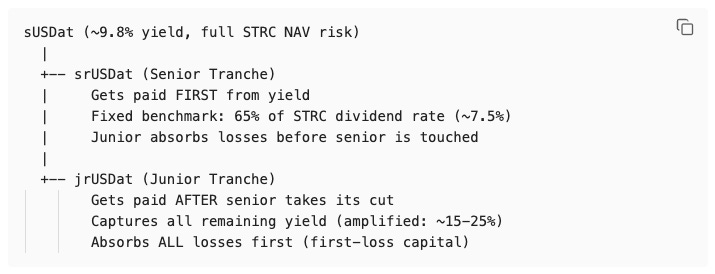

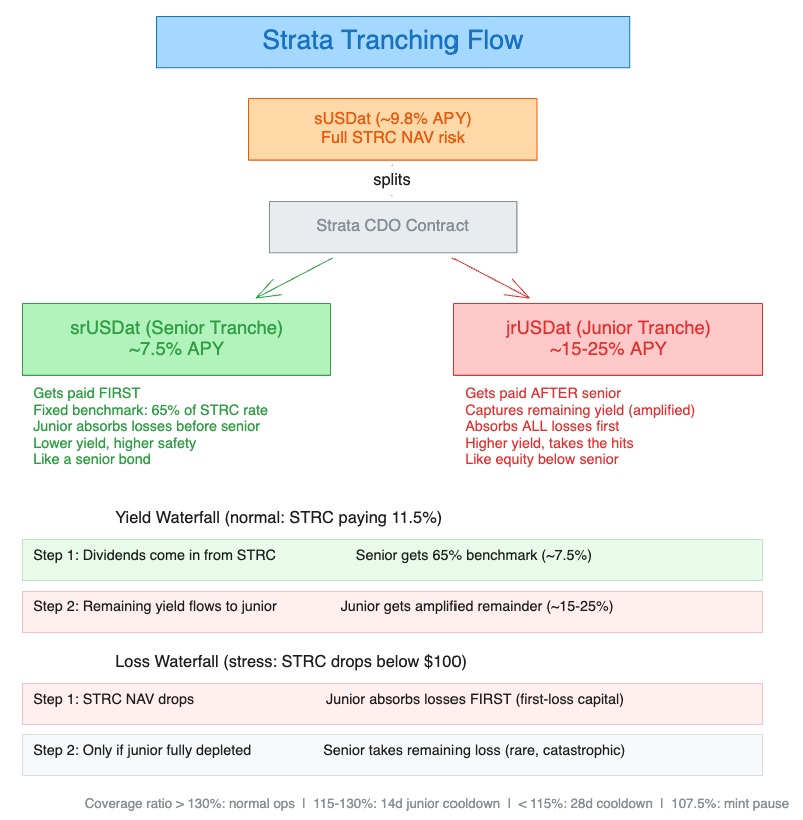

Layer 3: Strata Markets (Yield Tranching)

This is where Saturn gets genuinely innovative.

Strata takes sUSDat and splits it into two tranches -- like Wall Street structured credit, but on-chain and transparent.

Senior is like a senior bond -- lower yield, higher safety. Junior is like equity below the senior -- higher yield, takes all the hits.

The yield split adjusts dynamically based on how much capital is in each tranche. For Saturn, the risk premium is 100% -- junior absorbs the ENTIRE difference between actual yield and the senior benchmark.

What happens in different scenarios:

Scenario srUSDat gets jrUSDat gets Normal (STRC at par) ~7.5% ~15-25% STRC dividend cut 50% ~3.7% Near zero or negative STRC crashes, dividend paused 0% (but junior absorbs NAV loss first) Heavy losses STRC runs hot, 15% yield ~7.5% (capped) All the upside (~30%+)

This is literally how mortgage-backed securities worked (and blew up in 2008). The key differences: this is transparent, on-chain, and the “mortgages” are a single asset (STRC). Simpler, which is both better and worse -- better because you can see everything, worse because there’s no diversification. One asset, one point of failure.

Layer 4: Morpho (Leverage + Looping)

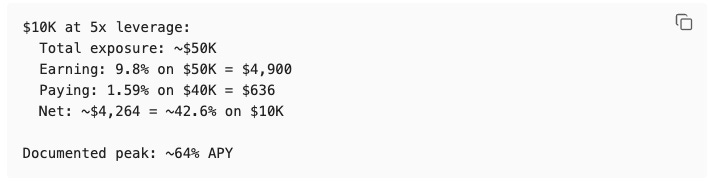

The leverage engine. Post sUSDat as collateral on Morpho, borrow USDC at ~1.59%, convert back to sUSDat, redeposit, repeat.

What kills the loop: sUSDat drops in NAV (STRC price falls). At 5x leverage, a ~15-20% STRC drop could trigger liquidation. The 64% APY comes with real wipeout risk.

The safer variant: PT-USDat as collateral instead. Treasury-backed, more stable collateral. Lower yield (8.91% - 1.59% = ~7.32% before leverage). At 3x: ~22% APY with lower liquidation risk.

Layer 5: Combination Strategies

The Conservative Stack (no STRC risk): PT-USDat on Pendle (8.91% fixed) + Curve LP USDC/USDat (20x points). Zero STRC exposure. Pure T-bill yield + points farming.

The Full Stack (protected yield + points): Stake USDat -> sUSDat -> Strata srUSDat -> Pendle LP (7.5x points + 16.2% APY). Senior tranche protects from first losses.

The Degen Stack: YT-USDat (30x points, principal decays) + sUSDat Morpho loop (64% APY). Max points + max yield, max risk.

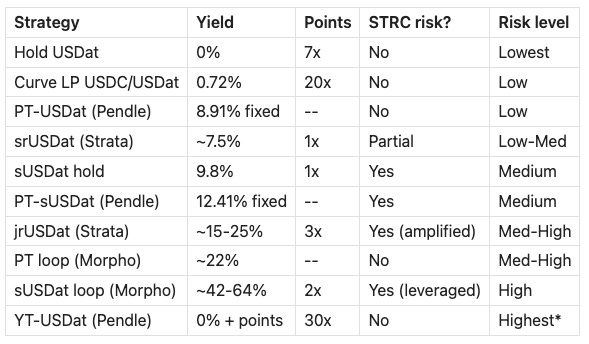

All Strategies Ranked

YT-USDat: no STRC risk but 100% principal loss at maturity by design.

The Points Game

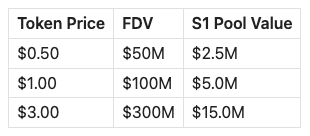

Saturn runs Season 1 Gravity Points from April 8 to August 8, 2026 (or $500M TVL, whichever first). The Saturn Foundation may allocate up to 5% of initial token supply to S1 participants.

The catch: the token doesn’t exist yet. No name, no supply, no TGE date. Points “have no monetary value and are not redeemable for cash. Saturn reserves the right to modify the program at any time.”

If we assume a $100M FDV and 5% allocation:

Compare: Apyx has 100M fixed supply, 5% to S1, 4% to S2, TGE timeline visible. Saturn is a black box on the most important variable.

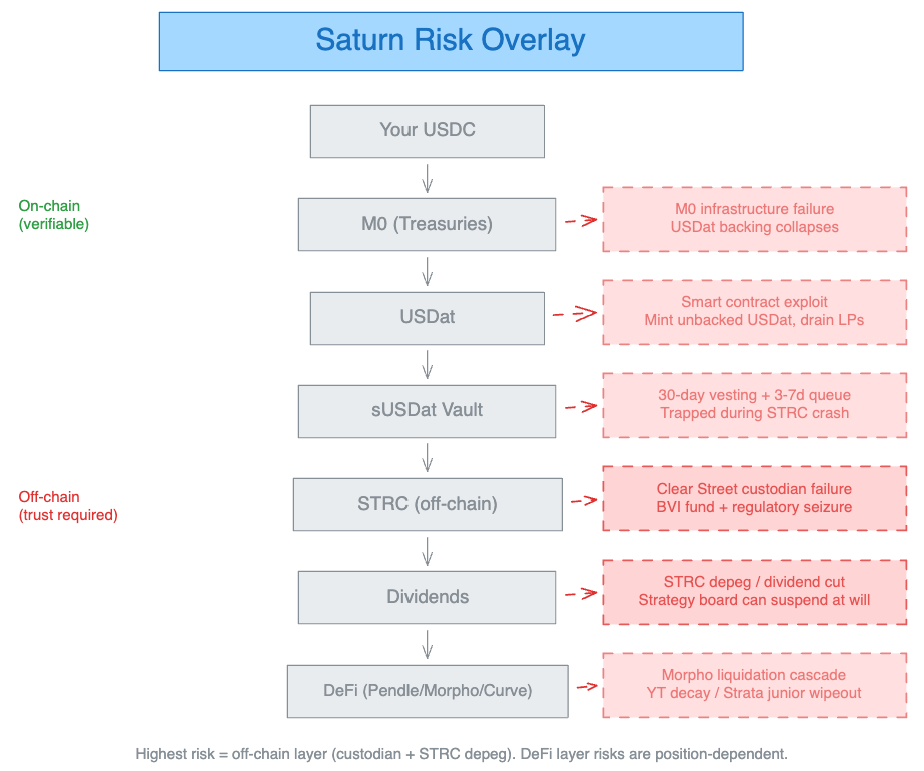

The Risks -- The Part You Actually Need to Read

Saturn is custodial at its core, like every STRC tokenizer. STRC sits off-chain in a BVI professional fund, custodied by Clear Street, administered by Securitize.

The difference: USDat capital (Treasuries) is on-chain and verifiable via M0 contracts. Saturn’s stablecoin layer is more transparent than competitors. The STRC custody layer carries the same risks as everyone else.

Tier 1: Structural Risks

STRC depeg / Strategy stress. STRC hit $90.52 before. Strategy can cut dividends. The dynamic reserve allocation provides a buffer -- but it also means yield drops to zero faster than competitors.

sUSDat demand collapse post-airdrop. 9.8% yield is below Apyx’s 13%. If the token disappoints and yield stays lower, capital migrates.

Custodial / counterparty risk. Clear Street and Securitize are the off-chain trust anchors. Accountable provides real-time proof-of-reserves (better than monthly attestations), but the BVI fund structure still means trusting a legal entity.

Tier 2: Position-Specific Risks

3-7 day withdrawal queue. Better than Apyx’s 20 days. But in a STRC crash, everyone exits simultaneously. Settlement could extend.

Morpho loop liquidation. 5x leverage + STRC price drop = wipeout.

Pendle YT decay. 30x points sounds great until your principal hits zero at maturity.

30-day yield vesting. Exit before 30 days, lose unvested yield. A gotcha competitors don’t have.

Tier 3: Tail Risks

Death spiral. BTC crash -> STRC below $85 -> dynamic reserve flips to 0% STRC -> yield drops to zero -> mass exits -> protocol sells STRC into a falling market -> NAV drops further.

Multi-protocol cascade. Saturn + Apyx + xStocks = $260M+ of on-chain STRC. All flowing through Pendle, Morpho, Curve. Five protocols deep on leverage loops. If one breaks, they all feel it. Nobody’s pricing the correlation.

What’s NOT a Major Risk

USDat depeg from smart contract hack -- Treasury-backed via M0. Even if Saturn’s contracts are exploited, the M0 backing remains

Audit risk -- Three Sigma + Certora audits completed. Strata has Cyfrin guardian

Team rug -- Kevin Li is public-facing, presented alongside Saylor. $3.1M raised, $105M TVL

Yield Comparison

PT-USDat at 8.91% on Treasury-backed collateral. That’s 2x what any T-bill fund pays, with no STRC downside. The premium exists because Gravity Points demand inflates USDat prices, creating a discount on PTs. You’re getting paid for other people’s speculation.

My Take

Saturn is architecturally better than Apyx. The clean separation between USDat (Treasury-backed, zero STRC risk) and sUSDat (full STRC exposure) is a genuinely smarter design. You choose your risk. Apyx blends it all together -- you can’t hold apxUSD without STRC downside. Saturn lets you.

The dynamic reserve allocation is the other thing nobody’s talking about. When BTC drops and Strategy gets overleveraged, Saturn auto-shifts reserves to Treasuries. Yield drops to zero but your principal is protected. Apyx doesn’t have this. In the next STRC stress event, this difference matters.

But better design doesn’t mean better returns. sUSDat pays 9.8%. apyUSD pays 13%. That’s a 30% yield gap.

The Binance question.

YZi Labs incubated Saturn. Spartan led seed. Susquehanna participated. This is a Binance-aligned project, and historically YZi Labs projects have a higher chance of getting listed on Binance. That’s the bull case.

The flip side: Binance Labs typically holds a token allocation, and there’s often a requirement to airdrop tokens to Binance holders (BNB stakers, Launchpool, etc.). That dilutes the pool for everyone else farming Gravity Points. You’re farming alongside Binance’s distribution machine, not ahead of it. Whether the listing premium outweighs the dilution depends on the tokenomics they haven’t revealed yet.

Structured credit is on-chain now.

Strata’s tranching of sUSDat into srUSDat (senior) and jrUSDat (junior) is literally how Wall Street structured credit products work. Senior gets paid first, junior absorbs losses. The 2008 version was opaque and built on garbage mortgages. This version is transparent, on-chain, and built on a single asset (STRC). Simpler, which is both better and worse -- better because you can see everything, worse because there’s no diversification. If STRC breaks, the entire tranche structure breaks with it. One asset, one point of failure.

Still -- the fact that you can now choose your risk tier on STRC yield (senior at 7.5% protected, junior at 15-25% leveraged, or raw sUSDat at 9.8%) is a real innovation. This is what DeFi composability is supposed to enable.

(im so fking proud of defi rn)

The contagion nobody’s pricing.

Saturn + Apyx + xStocks = $260M+ of on-chain STRC exposure. All flowing through the same pipes -- Pendle for fixed/variable yield splitting, Morpho for leverage loops, Curve for swap liquidity. Five protocols deep, stacked on top of each other. If Pendle has a smart contract issue, both Saturn and Apyx TVL takes a hit simultaneously. If STRC depegs hard, every protocol in this stack liquidates at once. The Morpho loops (5x leverage on STRC-exposed collateral) are the accelerant.

I am not saying it will blow up, I don’t think it will blow up but

This isn’t a Saturn-specific risk. It’s an STRC ecosystem risk. And we have to start pricing the correlation because each protocol’s risk section only talks about itself.

Who this is actually for.

Saturn serves more investor profiles than any other STRC tokenizer because of the clean separation:

“I want yield but I don’t trust STRC” -- PT-USDat on Pendle. 8.91% fixed, Treasury-backed, zero STRC exposure. 2x what any T-bill fund pays. The premium exists because other people’s points farming inflates USDat’s price. You’re getting paid for their speculation.

“I want STRC yield but not the full downside” -- srUSDat via Strata. ~7.5%, junior absorbs losses before you do.

“I want the yield” -- sUSDat at 9.8%. Straightforward, 3-7 day exit.

“I want to get degen” -- Morpho loop at 42-64% APY. You know the risks.

“I just want points” -- Curve LP USDC/USDat at 20x multiplier. Stablecoin pair, minimal IL.

The terms problem.

Saturn’s token doesn’t exist yet. No name, no supply, no TGE date. “Up to 5% of initial token supply” with a disclaimer that Saturn “reserves the right to modify the program at any time.” Compare that to Apyx: 100M fixed supply, 5% to S1, 4% to S2, timeline visible.

This cuts both ways. TVL is $105M vs Apyx’s $277M -- so if the token allocation is similar, each dollar of Saturn farming gets ~2.6x more points share. Lower TVL = better farming economics, IF the token materializes at a decent valuation. But the team can adjust terms anytime, and you’re farming blind on the most important variable.

My position: this is a “why not” farm, not a “go hard” farm. PT-USDat for the yield floor. Curve LP for the points. $5-10K to test. Scale up when the token details drop and the protocol survives its first real stress event.

Six weeks old. Untested in a drawdown. Token is a black box. Don’t be the one who sized up before the rules were clear.

Not financial advice. DYOR.